Deemed rejection, hard-blocked GSTR-3B, and the end of provisional ITC mean SMEs can no longer file first and reconcile later. Here is what actually changed, what you can fix yourself, and where the pipeline engineering gets real.

The 14th to the 20th

Every month, between the 14th and the 20th, someone in your office — or your CA's office — is downloading a GSTR-2B JSON, exporting a purchase register from Tally to Excel, and running VLOOKUPs to figure out which invoices match, which ones are close, and which ones are missing entirely.

Six days. That is the IMS review window. Every inbound invoice your suppliers filed in their GSTR-1 by the 11th shows up in your GSTR-2B on the 14th. You have until the 20th to accept, reject, or leave them pending before you file GSTR-3B.

Until March 2026, leaving invoices alone was fine. Silence meant acceptance. Your ITC flowed through.

That changed on April 1, 2026. Silence now means rejection. An invoice you did not explicitly act on in IMS is deemed rejected, does not appear in your GSTR-2B, and your ITC on it is gone. Claim it anyway and you face reversal with 18% per annum interest under Section 50(1) of the CGST Act (rate per the current notification, applicable on gross ITC wrongly availed).

This is not a policy tweak. This is a structural inversion of how ITC works in India.

Three Things Broke Simultaneously

April 1 did not bring one change. It brought three, and they compound.

Deemed rejection replaced deemed acceptance. Every invoice you receive now requires an affirmative action in IMS. For a business processing 200 purchase invoices a month, that is 200 accept/reject decisions in a six-day window. Miss five because a vendor filed late or your accountant was sick on the 18th, and those five invoices vanish from your GSTR-2B.

GSTR-3B filing is now hard-blocked. If the ITC you claim in GSTR-3B exceeds the ITC reflected in your GSTR-2B, the portal will not let you file. Not a warning. Not a notice. The submit button does not work. A single non-filing supplier can prevent you from filing your own return.

Provisional ITC is dead. Section 16(2)(aa) enforcement means ITC on invoices where your supplier has not filed their return reflecting the supply is now blocked — the 45-day timeline applies per the CGST Rules for determining supplier default. The old buffer — claim first, reconcile later — no longer exists.

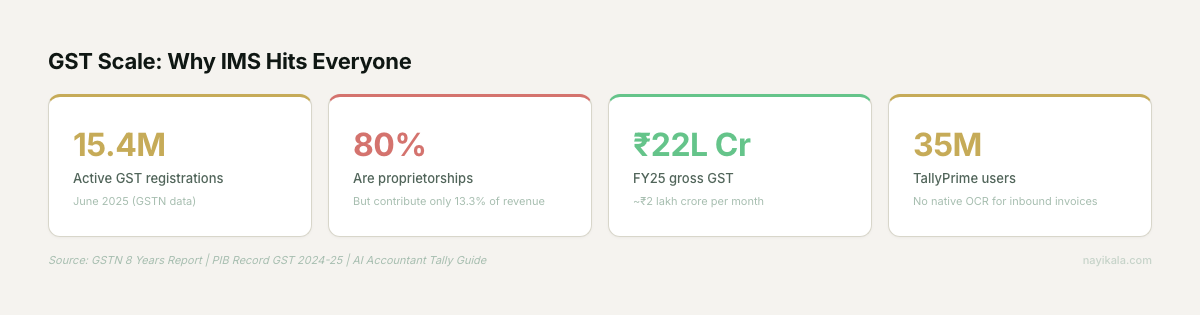

The businesses we have seen hit hardest are not the ones with bad processes. They are the ones with 50-100 vendors, a mix of compliant and non-compliant suppliers, and a CA handling 40 other clients simultaneously. A sole-proprietor CA in a Tier-2 city charging Rs 3,000 per month per client does not have the economics to run deep reconciliation on each one. The practical approach has been: file based on whatever appears in GSTR-2B and accept the ITC leakage as throughput cost.

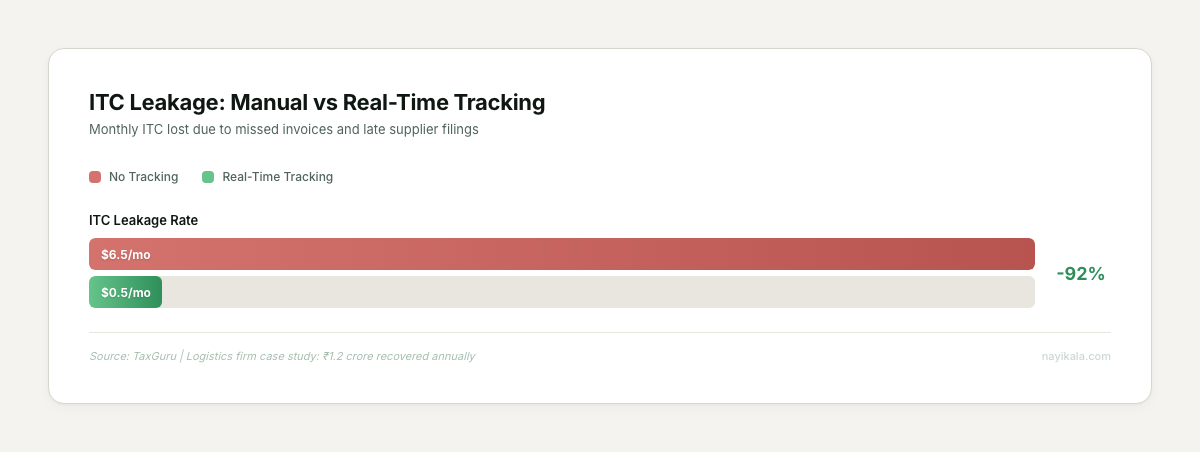

That leakage adds up. The businesses we have built reconciliation pipelines for lose 5-8% of expected ITC per month to missed invoices — supplier late filings, invoices that land after the 11th cutoff, GSTIN mismatches between HQ and branch registrations. For a firm expecting Rs 50 lakh in monthly ITC, a 20% vendor delay rate means Rs 10 lakh frozen every month. At 18% interest, that is Rs 1.8 lakh per year in pure financing cost on money you were owed.

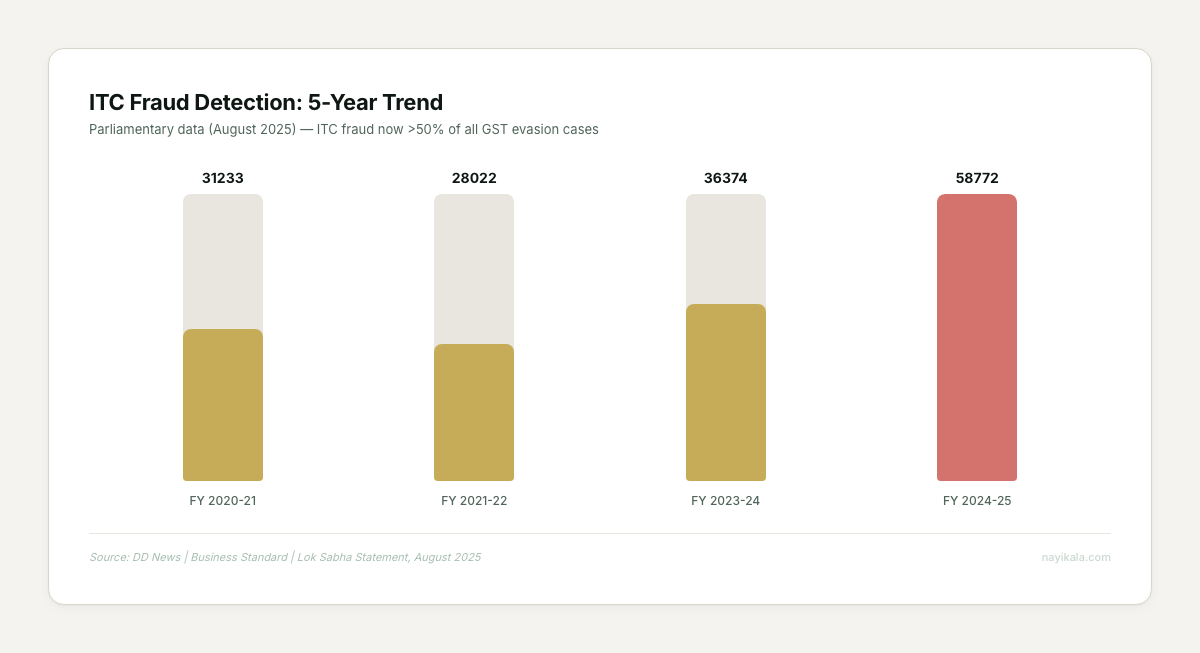

And the government is watching more closely now. DRC-01C notices under Rule 88D fire automatically when your GSTR-3B ITC exceeds GSTR-2B ITC by more than Rs 1 lakh or 20%, whichever is lower — thresholds set in CGST Notification 56/2023 (subsequently amended). You get seven days to respond. Non-response blocks GSTR-1 filing for subsequent periods — a cascading mismatch that takes months to unwind.

What You Can Do Monday Morning

Before you evaluate any software or talk to any vendor, do three things this week.

Map your actual mismatch rate

Pull your last three months of GSTR-2B and compare against your Tally purchase register. Count the invoices in each bucket: exact match, value mismatch, supplier-side missing, book-side missing. If you are below 100 invoices a month, this takes an hour in Excel. The number you are looking for is: what percentage of your expected ITC did you actually claim?

Most businesses have never measured this. The ones who have are usually unpleasantly surprised.

Score your vendors by filing reliability

Export your GSTR-2A/2B data for the last six months. For each supplier GSTIN, note which months their invoices appeared on time (by the 14th) and which months they were late or missing. You will find that vendor non-compliance is not random — it clusters. The businesses we have done this exercise with find that 10-15% of their vendors cause 80% of their reconciliation pain.

Once you know which vendors are unreliable, you can have a specific conversation with them. "Your GSTR-1 for March was filed on the 18th, which means our ITC was blocked" is a very different conversation from "please file on time."

Set up an IMS review calendar

Block 30 minutes on the 15th and 16th of every month for IMS review. Do not wait until the 19th. The businesses that file GSTR-3B without issues are the ones that start acting on IMS invoices the day GSTR-2B drops, not the ones scrambling on the deadline.

If you are doing fewer than 50 invoices a month, this manual discipline is enough. You do not need automation. You need a process.

Where It Gets Harder

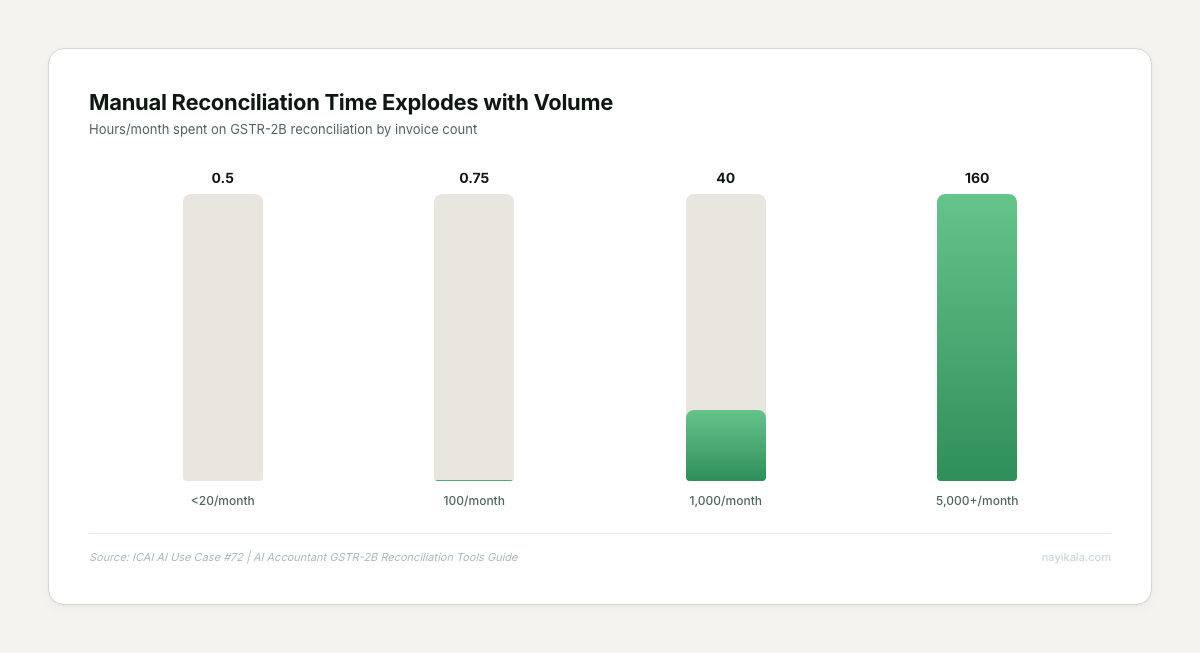

At 200 invoices a month, the manual process starts cracking. At 500, it breaks. At 1,000, you are spending 4-8 working days per month on reconciliation alone — and that is before you chase vendors or handle exceptions.

The instinct is to buy an OCR tool. Scan the invoice, extract the fields, push it into Tally. The vendor pitch sounds clean.

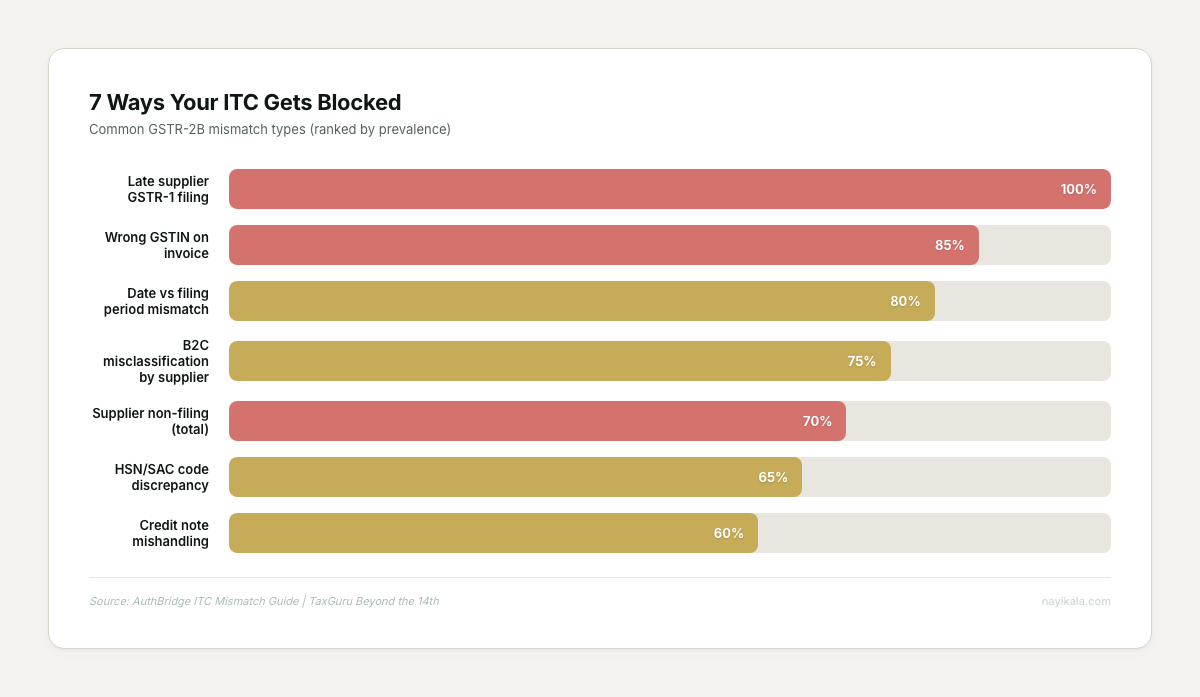

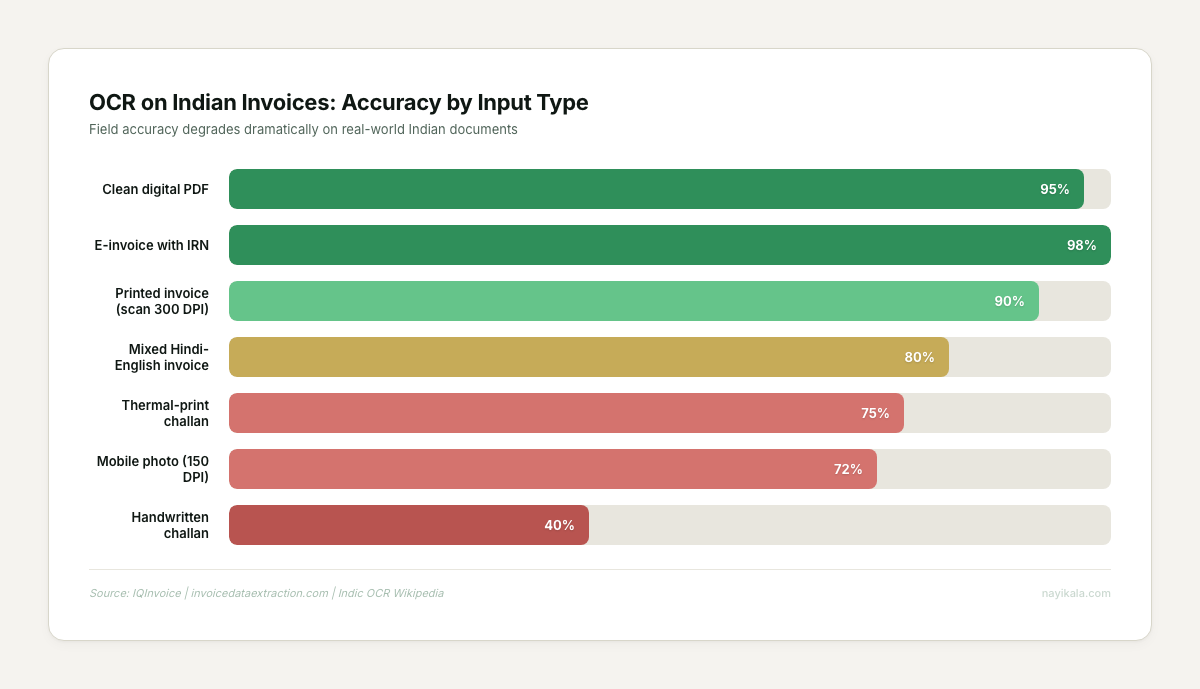

The reality is messier. In the OCR pipelines we have built for Indian invoices, we see a persistent 10% exception floor that vendors do not talk about in demos. At 500 invoices a month with 10 fields each, that is 5,000 extractions. At 90% accuracy, 500 fields need manual correction — comparable to the manual effort you were trying to eliminate. GSTIN extraction confuses O and 0, I and 1. Thermal-print challans fade within weeks. Mixed Hindi-English invoices break at script boundaries. Mobile photos of invoices run at 70-75% accuracy versus 95%+ for clean digital PDFs.

The real engineering problem is not OCR accuracy. It is what happens after extraction. The GSTIN needs checksum validation. The HSN code needs to match the GSTN dropdown exactly — manual entry was phased out on the GST portal starting late 2024/early 2025 per GSTN advisories. The tax amounts need decimal-level precision because a Rs 1 rounding difference, multiplied across hundreds of invoices, triggers DRC-01C. The vendor name needs fuzzy matching against your ledger master because "ABC Corp" and "ABC Corporation" and "A B C Corp" are the same vendor but three different strings.

Then the matched data needs to flow into your ERP as purchase vouchers, reconcile against GSTR-2B with tolerance rules for rounding, generate an exception queue for mismatches, and produce a validated ITC figure for GSTR-3B — all within that six-day window between the 14th and the 20th.

And that is just inbound. Outbound, your GSTR-1 data now hard-locks into GSTR-3B. Errors in outward supply fields cannot be corrected in GSTR-3B anymore — they have to route through GSTR-1A, which you get once per tax period. The margin for error on both sides of the ledger just went to near zero.

The vendor compliance layer is where most automation projects stall. You can automate your own data pipeline perfectly and still lose ITC because your supplier filed late, used the wrong GSTIN, or classified a B2B transaction as B2C. Building a vendor risk-scoring system that predicts filing behavior based on historical patterns, and triggers follow-up workflows before the 11th deadline rather than after — that is a different class of problem from scanning invoices.

The pipeline design — from OCR extraction through GSTIN validation, fuzzy vendor matching, tolerance-based reconciliation, IMS action routing, and GSTR-3B auto-population with hard-block-aware guardrails — is where the real engineering decisions live.

Related reading

← All posts