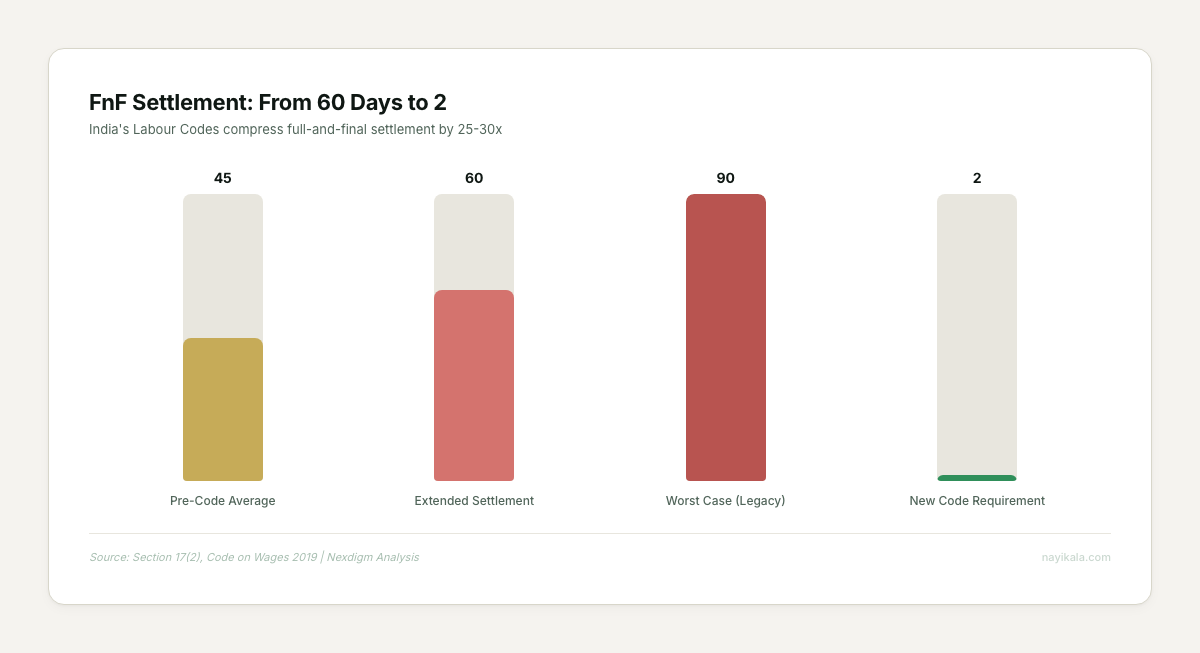

India’s new labour codes compress full-and-final settlement from 60 days to 2. The problem is not speed — it is that FnF is a distributed transaction across systems that were never designed to talk to each other.

Someone Resigns on a Thursday Afternoon

Your operations lead puts in her papers at 3 PM. HR gets the email, forwards it to the reporting manager, who is in a client meeting until 5. The next morning, someone opens the HRMS to check her leave balance. Payroll needs her last working day confirmed. Finance wants to know if there is a laptop recovery pending. The manager finally approves the resignation on Monday.

Under the old regime, none of this mattered much. Full-and-final settlement happened in 45 to 60 days. Sometimes 90. There was time to collect approvals, reconcile leave, compute gratuity, run it past the CA, and cut the cheque in the next payroll cycle.

That ended on April 1, 2026.

Section 17(2) of the Code on Wages, 2019 — now fully operational — requires all wage components to be settled within two working days of an employee’s last day. Not two weeks. Not the next payroll run. Two working days.

The businesses we work with did not panic about this because of the penalty amounts — a first offense fine of INR 10,000-20,000 is manageable. They panicked because their payroll runs on batch cycles, and a batch system has no concept of a resignation event.

The 25x Compression Nobody Planned For

Here is what FnF actually requires you to compute, in sequence, before that 48-hour window closes:

Unpaid salary, pro-rated to the last working day. Sounds simple until you realize the divisor — 26 days or 30 days — is a source of disputes and your system may not even have the last working day confirmed yet.

Leave encashment, which means your HRMS leave balance must be locked at the exact resignation timestamp. If a manager approves a late leave credit after resignation but before settlement, you have a race condition. The tax exemption on this component was raised to INR 25 lakh in Budget 2023, so the TDS math changed too.

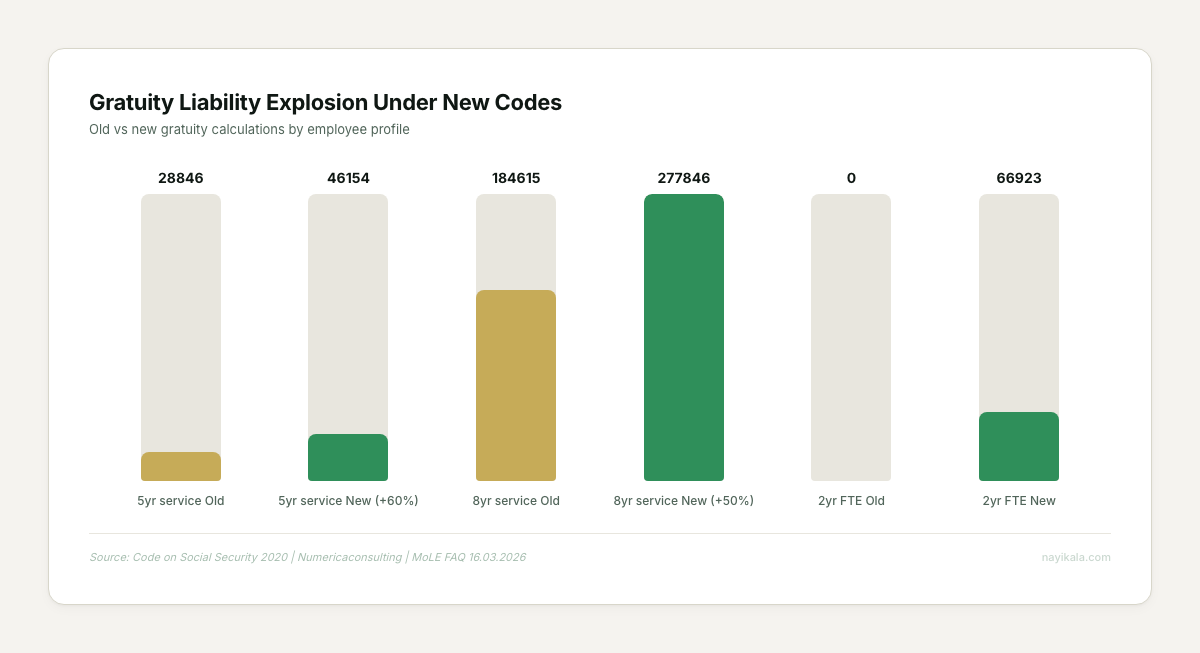

Gratuity, now payable after just one year of service for fixed-term employees — it was five years before. A 2-year contract employee who was previously ineligible now generates a gratuity liability. Across the businesses we have restructured for this, the gratuity liability increase runs 25-60% depending on workforce composition.

Pro-rata bonus, which is structurally uncomputable at resignation time. Bonus is calculated on allocable surplus for the April-March year. If someone resigns in August, the surplus is unknown. You either estimate and risk under/overpayment, or defer and arguably violate the spirit of the 48-hour rule.

TDS computation, which requires projecting annual tax liability across all FnF components minus declared deductions. And here is the timing trap: the Income Tax Act 2025 replaced the Income Tax Act 1961 on the same date — April 1, 2026. Section numbers changed. Form 16 became Form 130. Form 24Q became Form 138. A March resignation with April settlement crosses two tax law boundaries simultaneously.

Notice period recovery, requiring the contractual notice period, actual last working day, and manager waiver status — three data points that may live in three different systems.

This is not a speed problem. This is a distributed transaction across systems that were never designed to execute together, and they now have a 48-hour SLA.

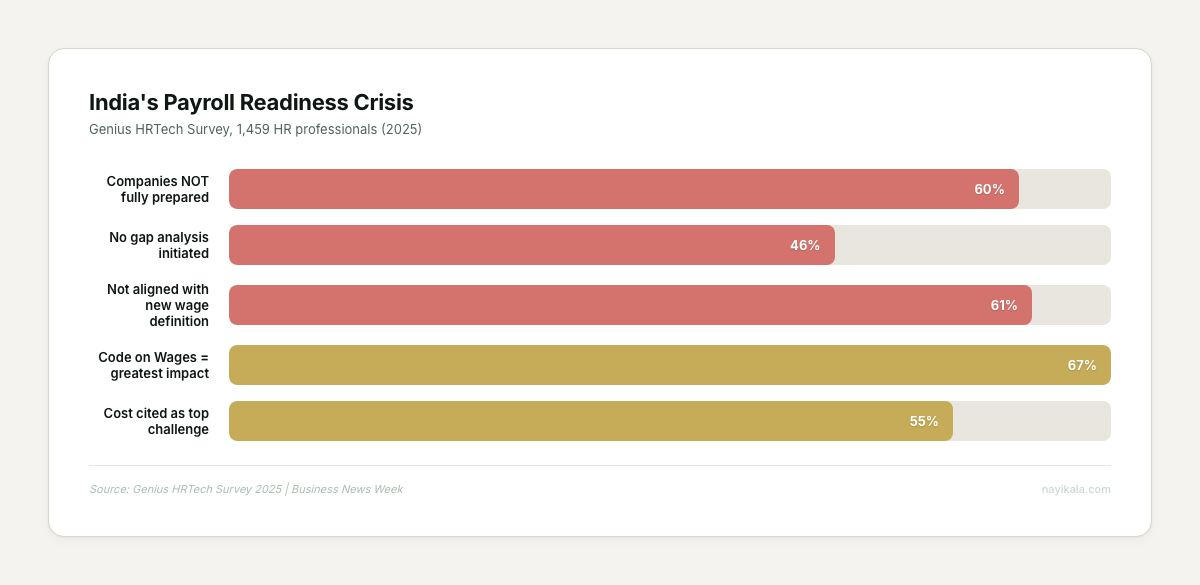

According to a Genius HRTech survey of 1,459 HR professionals in 2025, 60% of companies are not fully prepared for the new labour codes. 46% have not even begun a structured gap analysis. 61% are still not aligned with the revised wage definition — the rule that basic plus DA must constitute at least 50% of total remuneration, which changes the PF contribution base for every employee whose CTC was structured around inflated allowances.

What You Can Do Monday Morning

Before touching any software, map what you actually have.

Step 1: Time your current FnF. Pick the last three resignations. Note the resignation date, the date FnF was computed, and the date it was paid. If you are averaging 30+ days, you know the gap.

Step 2: List every system that touches FnF. HRMS for leave balances. Payroll software for salary and TDS. A spreadsheet or ERP for asset recovery. Email threads for manager approvals. The EPFO portal for PF. State portals for professional tax. Count them. The businesses we have mapped typically hit 6 to 8 separate systems for a single FnF.

Step 3: Check your wage definition. Pull five offer letters. Calculate basic plus DA as a percentage of CTC. If it is below 50%, your PF contributions are being computed on the wrong base. One company we worked with brought 34 employees to the 50% basic floor and saw employer PF costs rise by INR 1.87 lakh per month. This is not optional — it is the law now.

Step 4: Audit your gratuity liability. Under the new codes, fixed-term employees are eligible after one year, not five. If you have contract staff who have crossed 12 months, they have a gratuity entitlement that may not be provisioned. Under Ind AS 19, the entire liability increase hits your P&L as Past Service Cost — it should already be in your March 31, 2026 financial statements.

Step 5: For one week, track every resignation-related communication. Note where it starts (email, verbal, HRMS), who it goes to, and how long each handoff takes. The bottleneck is almost never computation. It is approval routing.

These five steps cost nothing. They give you the diagnostic. And for most businesses under 50 employees, tightening the approval chain and pre-computing leave balances weekly gets you from 45 days to under 10 without buying anything.

Where It Gets Harder

Getting from 10 days to 2 is a different problem entirely.

Batch payroll — the architecture that runs monthly, processes everyone at once, and produces a single output — has no mechanism to trigger on a resignation event. It cannot lock a leave balance atomically at resignation time. It cannot produce a final tax computation mid-period. The 48-hour mandate is not asking you to run batch faster. It is asking you to run a fundamentally different architecture.

The pattern that solves this is event-driven: a resignation creates an event, that event triggers a sequence — lock leave balance, calculate gratuity, compute TDS, generate settlement, route for approval, disburse payment. Each step has a compensating action if it fails. But the last step — payment disbursement — has no compensation. Once the money moves, it has moved. This is the saga pattern, and the failure modes are specific: dirty reads during rollback, lost updates from concurrent FnF processing if two people resign on the same day, idempotency violations that cause double payment.

Then there is the portal integration load. A national employer with operations in five or more states files across 12 to 15 distinct government portals — EPFO, ESIC, TRACES, state professional tax portals for each of the 21 states that levy PT, state labour welfare fund portals, Shram Suvidha. Each with its own authentication, its own filing schedule, its own reconciliation logic. The FnF clock does not pause while you wait for portal confirmations.

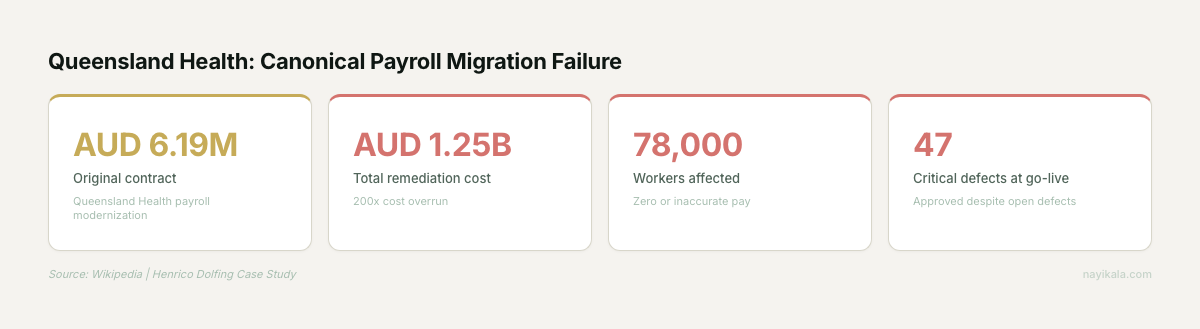

Globally, payroll accuracy sits at 78% — one in five runs contains an error, according to ADP’s 2024 survey of 1,825 payroll leaders across 20 countries. 53% of companies reported being fined for payroll errors in the past five years (Strada 2024). Queensland Health in Australia migrated their payroll system, went live with 47 critical defects still open, and spent AUD 1.25 billion remediating a contract that started at AUD 6.19 million. Payroll migration done wrong is not an inconvenience. It is an existential event.

The real design decisions live in the event schema, the saga compensation logic, and the tax law boundary handling for cross-period settlements.

← All posts