Indian cafés are revolutionising two businesses at once. The one they run, and the one yours runs inside of them. Both come down to the same four percentages.

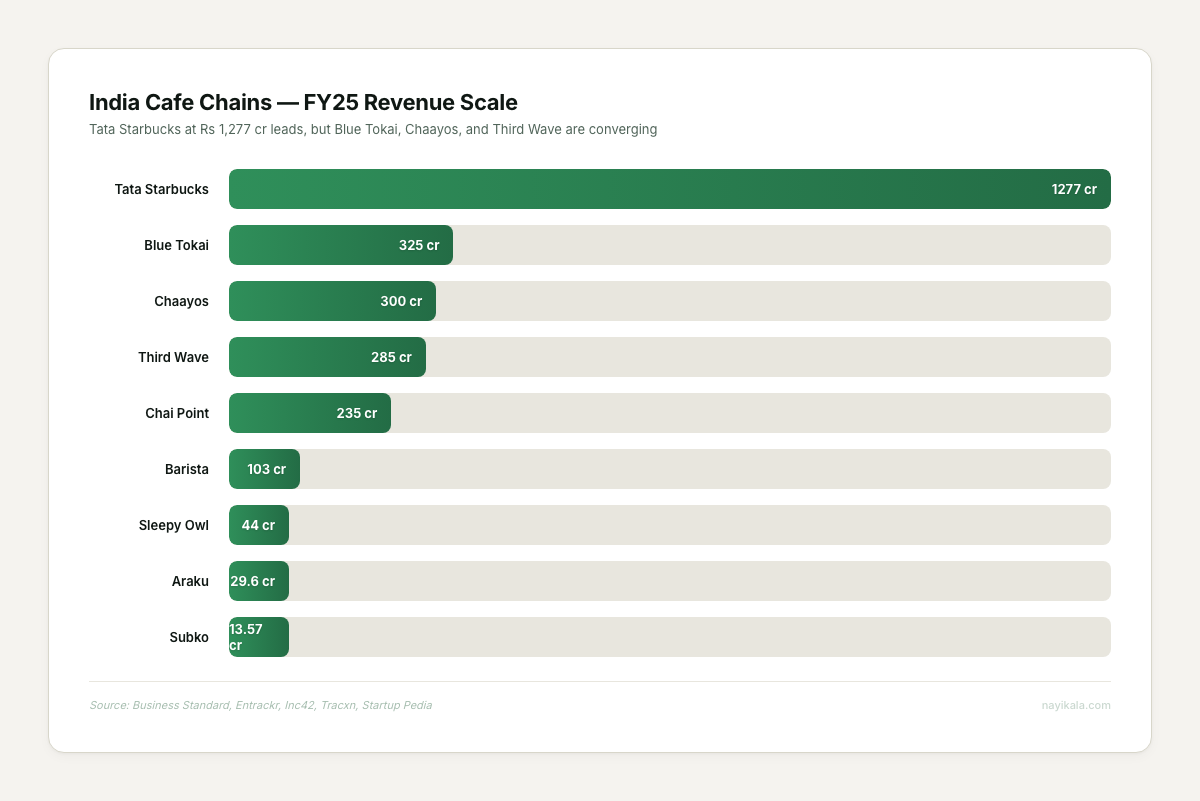

Third Wave Coffee spent ₹81.25 crore on rent in FY24 to earn ₹241 crore. Thirty-four paise of every rupee went to landlords before the first bean was roasted. In the same year, Chaayos paid roughly 6% of revenue in rent and turned EBITDA-positive by cutting expenses 11%, not by chasing growth. Both companies sell hot drinks to Indian office-goers. One is a rent-heavy loss engine. The other is a retention business. That gap is not a coffee story. It is an operations story, and it is the same story playing out in your 15-outlet sweets chain, your 20-person D2C brand, and the pizza parlour whose aggregator commissions eat 35% of the gross.

Then walk into the Costa at 4th Block Koramangala on any Wednesday at 3 PM. The ZipDial CEO once counted at least eight companies being started at that one outlet. Blue Tokai now has a formal partnership page with WeWork at bluetokaicoffee.com/pages/wework. Social Offline did ₹682 crore in FY24 on a "café by day, bar by night, coworking throughout" floor plan. The Indian café is simultaneously the hardest operations problem in retail and the default office for the companies that cannot afford a real one.

Two revolutions. Same spreadsheet.

The Operator Side: Rent, Retention, and the 34% That Killed Cafés

The Indian café unit economic is almost always decided by four percentages. Rent, labour, COGS, and aggregator commission. When you stack the FY24 numbers on top of each other, the winners and the losers separate cleanly.

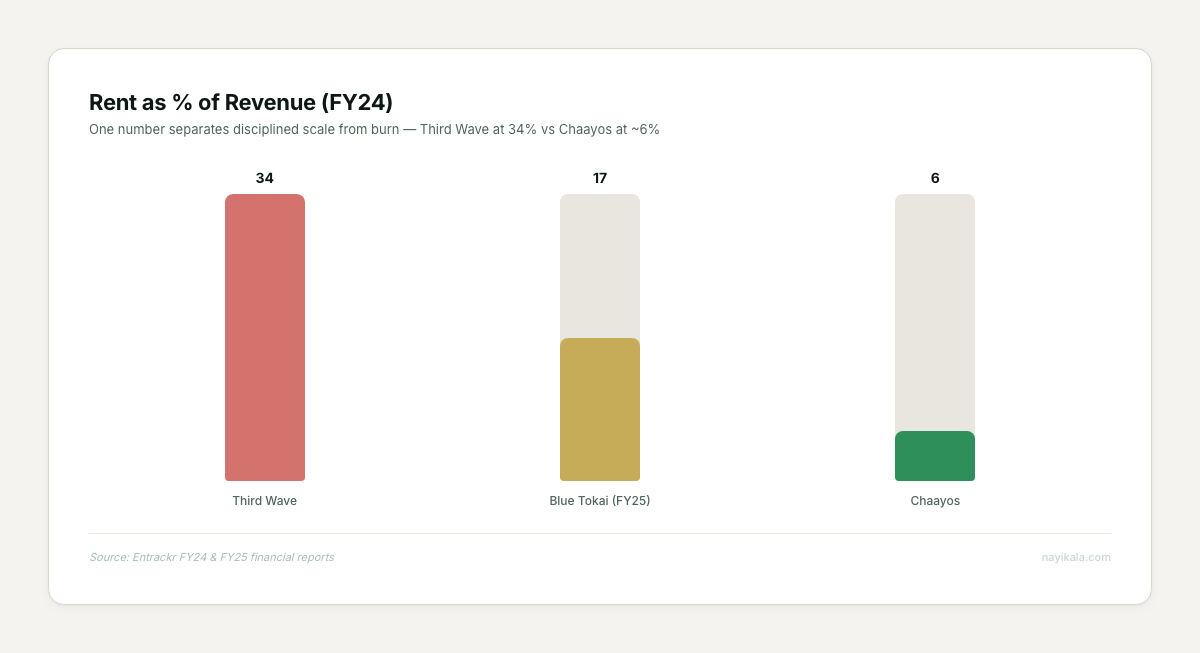

Chaayos FY24: rent ~6%, employees 33%, materials 31% per Entrackr's FY24 filing. Blue Tokai FY25: rent 17% (₹55.2 cr on ₹325 cr), employees 29%, materials 35% per Entrackr FY25. Third Wave FY24: rent 34%, employees 40%, materials 36%, EBITDA margin −35.52% according to Entrackr's FY24 filings. Third Wave was spending ₹1.48 to earn ₹1, and about 70% of its outlets were loss-making at the unit level.

The rent number alone tells you most of what you need to know. BKC rent hit ₹700 per square foot in 2024, the highest in India. Khan Market went from ₹700 to ₹1,300 between 2014 and 2019, then rose another 20% post-COVID per Business Standard's 2024 real estate tracker. In that environment, your choice of store footprint is your choice of business model. Blue Tokai made 90% of its outlets ~500 sq.ft. modular units. Third Wave built concept cafés. One ratio at 17%. The other at 34%. That's the whole movie.

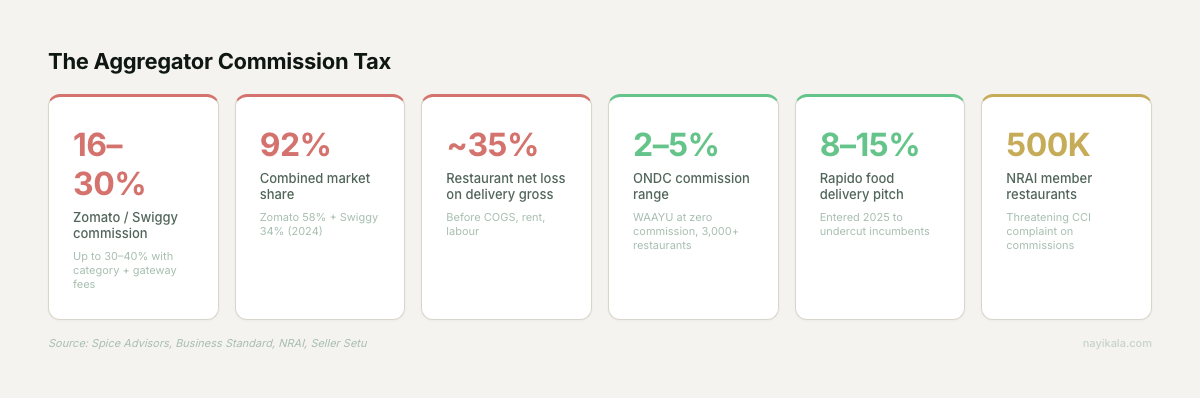

Then there's the aggregator tax. Spice Advisors' 2025 commission analysis pegs Zomato and Swiggy at 16–30% typical, climbing to 30–40% once category fees and payment gateway cuts stack up. On a delivery order, a restaurant loses roughly 35% of gross before it has paid for a single ingredient. NRAI has threatened a CCI complaint. ONDC is sitting at 2–5%. Rapido has pitched 8–15% to undercut the duopoly. The sellers we've seen surviving in food delivery are not picking one channel. They are running their own WhatsApp ordering funnel in parallel, tracking the commission delta per order per channel, and rebalancing monthly.

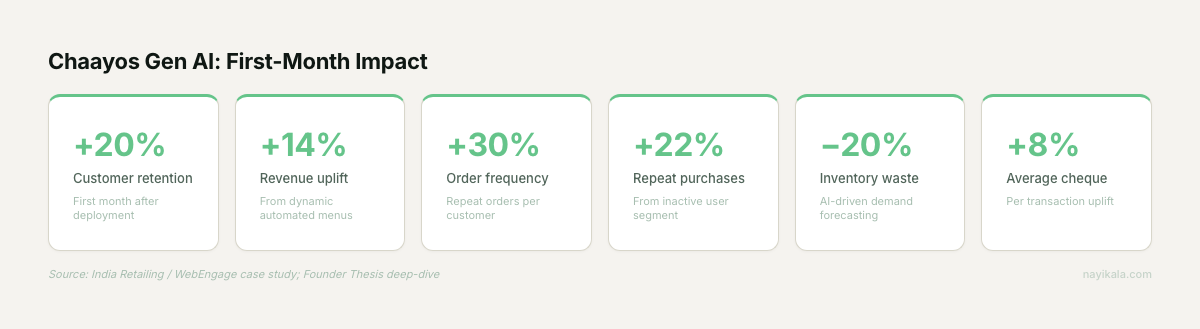

Chaayos's response was not cheaper rent. It was engineering. Roughly 20% of HQ budget goes to their in-house stack, Kettle POS and the Chai Monk IoT brewer, which drives ~80% of the brew process and enables 80,000+ drink combinations. Their Gen AI rollout cost ₹1.5 crore and, in month one, India Retailing documented retention +20%, revenue +14%, average cheque +8%, inventory waste −20%, and ratings 3.9 → 4.3. Their 95% loyalty enrolment via WebEngage moved repeat purchase from 44% to 51% per WebEngage's case study.

When rent is structurally locked at 15–25% and labour at 25–35% — the ranges we see across café P&Ls — retention is the only knob left that actually moves the business. Chaayos understood this before they expanded. Third Wave is learning it expensively.

The Infrastructure Side: The Office Has Dissolved

Now flip the spreadsheet. You are not the café. You are the 20-person Series A startup that used to sign a 5-year lease in Indiranagar and is not going to anymore.

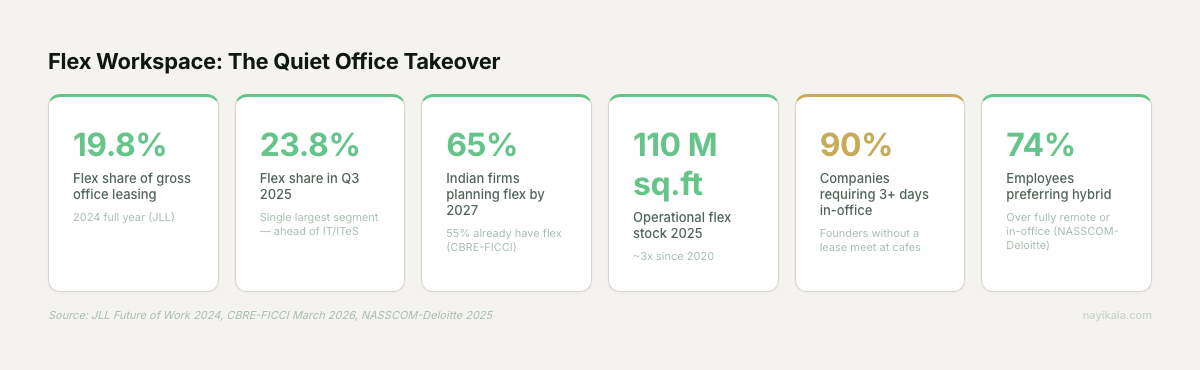

JLL's 2024 Future of Work survey found 90% of Indian companies require 3+ days in office, among the highest globally. But flex took 19.8% of India's gross office leasing in 2024, 15.3 million square feet, per JLL. In Q3 2025 flex overtook IT/ITeS as the single largest leasing segment at 23.8%. CBRE-FICCI's March 2026 "Flex-plosion" report projects 65% of Indian firms will use flex by 2027. Pune is compounding at 33% CAGR since 2019.

The monthly cost math is brutal and clean. A fixed desk in Bengaluru coworking runs around ₹9,000. Mumbai ₹16,000. A traditional fit-out metro seat is ₹9,800–₹21,700 once you amortize the capex. A café day-pass on myHQ is ₹200–₹1,500. For a founder doing two investor coffees a day, the café is operationally cheaper than the lease and socially denser than the coworking. So the "office" has stopped being a place. It is now a portfolio.

Cafés have read the demand signal and are pricing into it. Blue Tokai × WeWork is not a marketing co-brand. It is a formal listing — their Koramangala outlet has hot desks, meeting rooms, and quiet work zones bookable through myHQ. Social Offline built the model natively. Riyaaz Amlani's framing in The News Minute: "A café is accessible, approachable. You can go twice a week, maybe every day. Frequency of customer visits is higher." Higher frequency is a unit economics statement, not a hospitality one.

The productivity research backs the migration. The University of British Columbia and University of Virginia study, widely cited in HBR's 2017 synthesis, found 70 dB ambient noise, the typical café, measurably boosts divergent thinking. 85 dB hurts. Silence narrows. The café is an accidentally optimal environment for the kind of work a Series A founder actually does: pattern-matching across a pitch, a hiring plan, and a pricing sheet at the same time.

So the café becomes the deal venue, the meeting room, the vendor testing ground, and in the case of Social, literally the office. And the operational stack behind the café, Petpooja's 50,000+ F&B clients, UrbanPiper's ~8 lakh daily orders — 20% of India's online food orders — and Chai Point's Fountain platform running 3,500+ IoT dispensers, is quietly where the real margin is being captured. The businesses making money on the café revolution are not the cafés. They are the POS layers, the IoT platforms, the loyalty engines, the commission arbitragers.

What a 20-Person Company Should Actually Steal

You are not going to build a Chai Monk. You are also not going to sign a WeWork deal. The four percentages travel anyway.

Lock your four percentages and put them on a wall. Rent, labour, COGS/materials, commission or acquisition cost. Compute them monthly. If any one of them crosses the Chaayos-to-Third-Wave gap, you are no longer running the same business you were running last quarter. The pizza parlours we've looked at behind the dashboard: at 18% commission they're a margin business, at 28% they're acquiring customers for Zomato. Same storefront, different company.

Treat retention as the only infinite knob. The Chaayos number that matters is not the 80,000 combinations. It is that 95% of customers are in the loyalty program and repeat purchase moved from 44% to 51%. For a 20-person D2C brand, that means the WhatsApp flow that captures consent at the first order, tags the customer by SKU category, and re-pings them at the right interval is not a marketing project. It is the P&L.

Audit your channel commission tax this week. Pull 90 days of aggregator orders. Compute gross revenue, net revenue after commission, COGS per order, packaging, and delivery partner cost. If the net-net is below contribution-positive, you are paying Zomato to acquire a customer who may never come back. WAAYU has 3,000+ restaurants on the zero-commission ONDC rails. Rapido is live with 8–15%. The question is not whether to use aggregators. It is what share of orders you are willing to route through them while you build the direct channel.

Make the café part of your cost structure, honestly. If your team is meeting at Blue Tokai three times a week, it is an operating expense, not a perk. Budget it. Pick two or three anchor venues with reliable Wi-Fi, bookable meeting rooms, and a manager who recognizes your team. Social Offline, Blue Tokai × WeWork, Smaaash-style hybrids, and myHQ's café pass network are all priced for this. The founders we've seen scale from 10 to 40 people without a lease are not winging it. They have a rotation.

Where the Math Gets Harder

The uncomfortable layer is that the four percentages are not independent. Your commission ratio sets your pricing, which sets your AOV, which sets your repeat cadence, which sets your CAC payback, which sets how much rent or lease you can absorb. Chaayos's gen-AI system is not one tool. It is a data pipeline where the POS order, the loyalty identity, the inventory state, and the recommendation model all read and write against the same event stream. Starbucks's Deep Brew runs on Azure and decides cold-brew steep start times, labour allocation, and drink surfacing from one model.

The moment you try to wire your WhatsApp funnel, your Tally books, your Petpooja POS, your Zomato/Swiggy feeds, and your quick-commerce listings into one retention loop, you are no longer running marketing automation. You are running a small data platform with consent boundaries, idempotency requirements, and a PII retention policy under the 2025 labour and data regimes. The 50% basic-pay rule in the November 2025 labour codes alone has changed the labour percentage for every compliant chain overnight.

Most SMEs try to do this with four SaaS tools and a Google Sheet in the middle — the sheet is where the margin quietly evaporates, and the integration design, the event schema, and the consent model are where the real decisions live.

Related reading

← All posts